How to Choose the Right Funding Path

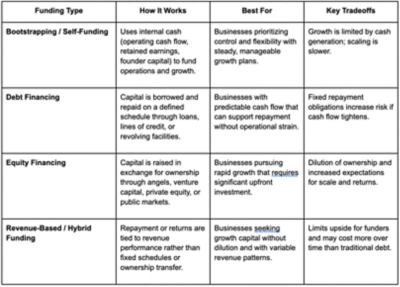

Choosing the right funding model is a decision about what the business can (or is willing to) trade in exchange for capital. It also shapes how to manage business cash flow as the company grows. Some models require fixed repayment. Others reduce founders’ ownership. Others preserve control but limit how quickly a business can scale.

The best path depends on which tradeoffs the company is positioned to absorb at its current stage. When evaluating funding options, business owners should consider:

Cash flow predictability: Businesses with stable, recurring revenue can typically support debt repayment schedules. Companies with uneven or early-stage revenue are better suited for equity or revenue-based models that don’t require fixed payments during growth periods.

Capital intensity of the growth plan: Debt is often better suited to investments with clear timelines and payback periods (e.g. building infrastructure), while equity is usually a better fit for longer-term growth initiatives (e.g. market expansion) where returns may take more time to materialize.

Tolerance for ownership dilution: Equity financing introduces new stakeholders who share in governance and decision-making. Founders who want to retain control may prefer debt or bootstrapping, even if growth happens more gradually.

Risk distribution: Debt concentrates risk in near-term cash flow through repayment obligations, while equity distributes risk across investors who will benefit only if the business grows successfully.

Future financing flexibility: Every funding decision affects the next one. Heavy debt can limit borrowing capacity later, while certain equity structures complicate future investment rounds or exits.

A strong funding decision matches the structure of the capital to the realities of the business—an alignment that’s crucial to future stability. When it’s wrong, costs show up later in repayment pressure or limited strategic options. But when it’s right, businesses are positioned to grow without constraining cash flow or future opportunities.

Unbalanced budgets lead to missed goals and lost opportunities. Achieve a 'just right' budget that motivates teams and protects your business by downloading this whitepaper.