Best Practices for Building Your AP Forecast

A strong forecast is shaped by the quality of your accounts payable process. Below are five actionable best practices to help you better manage cash flow and create forecasts that are more resilient, precise, and responsive to change.

1. Connect Data Across Functions

To build a complete forecast, integrate AP data with purchasing, procurement, and treasury systems. This helps you track your commitments before they become liabilities. For example, matching purchase orders to expected invoices can improve accuracy and reduce surprises.

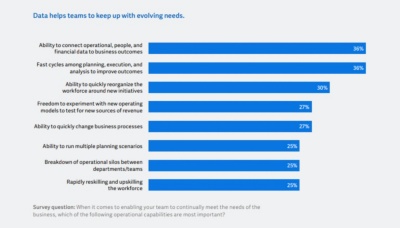

2. Model Multiple Scenarios

Don’t rely on a single version of the future. Model different outcomes based on changes in vendor payment terms, price fluctuations, or procurement volume. Identify which vendors offer flexibility and which are high-risk, and run sensitivity analyses to understand how changes impact your cash position.

3. Create Rolling Forecasts With Defined Update Cycles

Shift away from one-and-done forecasts. Use rolling forecasts instead, and update monthly or alongside your close process. Establish a cadence to revise inputs such as COGS, payment behavior, and vendor additions to keep projections current.

4. Use Historical Trends to Build Predictive Logic

Analyze payment behavior over time. What are your average payment lags by vendor? When do discounts typically go unused? Use that data to establish patterns that inform more reliable forward-looking estimates and build in alerts when deviations occur.

5. Align Forecasts With Procurement and Business Cycles

Coordinate your forecast with known procurement cycles, product launches, or seasonal shifts in demand. For example, if Q4 typically sees a spike in raw material purchases, your forecast should reflect the timing and volume of those expected payables. Similarly, align payment projections with supplier delivery schedules or promotional calendars to mirror how purchasing activity maps to actual cash obligations.

6. Review Forecast Accuracy Post-Close

After each monthly or quarterly close, compare forecasted AP against actual outcomes. Identify where you over- or under-estimated obligations, and document the drivers of those variances. This regular feedback loop will help you refine your assumptions and continuously improve your forecasting model.