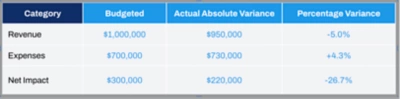

What Is Budget Variance?

Budget variance occurs when there’s a difference between a company’s financial plan and the actuals recorded in the budget sheet. At its simplest, it compares budgeted expectations to realized outcomes over a defined period.

But the real value of budget variance analysis lies less in the calculation itself and more in what the deviation reveals about the accuracy of financial forecasting models and the actions needed to remain aligned. In other words, variance isn’t inherently good or bad. Instead, the types of variance are divided into favorable or unfavorable.

A favorable variance may indicate disciplined cost control, or it could signal delayed hiring, postponed investments, or under-resourced teams that will feel pressure later. An unfavorable variance might reflect poor planning or weak execution, or it could be a result of intentional decisions, such as accelerating spend to capture a spike in demand.

Key insights gained from a budget variance analysis include:

- Assumption accuracy: Reveals where original planning assumptions no longer align with actual financial behavior over the period.

- Execution pacing: Surfaces whether spending or revenue realization is occurring faster or slower than expected.

- Demand signals: Highlights changes in volume, mix, or customer behavior that affect revenue performance.

- Cost structure pressure: Exposes areas where fixed or variable costs are drifting from plan.

- Timing effects: Distinguishes between temporary timing differences and structural changes that require plan adjustment.

For example: Coming in under the budgeted amount of operating expenses may initially look positive on paper. But if unfilled roles or deferred projects are driving the savings, the organization could be trading short-term efficiency for longer-term delivery risk.

Conversely, exceeding a quarterly expense budget may appear negative until it becomes clear that the overage came from pulling forward hiring to support stronger-than-expected demand. The goal in practice isn’t to eliminate variance, but to understand what it’s signaling early enough to respond.